If you run a business in Indonesia and compensate your employee with a bonus as a compliment to a regular salary, you have to deduct the tax from the payroll. As stipulated in UU PPh1, all payment types received by your employee, including wage/salary and bonus, are subject to national income tax law.

As an employer, you will calculate, withhold from the payslip, and remit employee tax to the government. Therefore, you better understand the bonus tax calculation according to the latest regulation, including the latest bonus tax rate.

Personal income tax in Indonesia: new rates and formula

The government has changed the rules to calculate income tax for resident taxpayers (PPh 21) by combining two types of rates called the effective rate and the progressive rate.

1. Average effective rate

Government Regulation 58/20232 introduces the average effective rates (TER) applicable for monthly withholding tax. The new rules simplify tax calculation as the rate applies directly to a monthly gross income. The formula is as follows:

Income Tax (PPh 21) Withholding = Effective rate x Gross income

So, what is the effective tax rate?

According to the regulation, the effective rates are 125 fixed rates categorized into three groups based on non-taxable income (PTKP). The Directorate General of Taxes classifies PTKP by marital status and the number of dependents.

- Category A for PTKP:

- TK/0 (unmarried with no dependents)

- TK/1 (unmarried with a single dependent)

- K/0 (married with no dependents)

- Category B for PTKP:

- TK/2 (unmarried with two dependents)

- TK/3 (unmarried with three dependents)

- K/1 (married with a single dependent)

- K/2 (married with two dependents)

- Category C for PTKP K/3 (married with three dependents).

| No | Category A | Category B | Category C | |||||

| Gross Income (Rp) | Rate | Gross Income (Rp) | Rate | Gross Income (Rp) | Rate | |||

| 1 | Up to 5,400,000 | 0,00% | Up to 6,200,000 | 0,00% | Up to 6,600,000 | 0,00% | ||

| 2 | 5,400,001 to 5,650,000 | 0,25% | 6,200,001 to 6,500,000 | 0,25% | 6,600,001 to 6,950,000 | 0,25% | ||

| 3 | 5,650,001 to, 5,950,000 | 0,50% | 6,500,001 to 6,850,000 | 0,50% | 6,950,001 to 7,350,000 | 0,50% | ||

| 4 | 5,950,001 to 6,300,000 | 0,75% | 6,850,001 to 7,300,000 | 0,75% | 7,350,001 to 7,800,000 | 0,75% | ||

| 5 | 6,300,001 to 6,750,000 | 1,00% | 7,300,001 to 9,200,000 | 1,00% | 7,800,001 to 8,850,000 | 1,00% | ||

| 6 | 6,750,001 to 7,500,000 | 1,25% | 9,200,001 to 10,750,000 | 1,50% | 8,850,001 to 9,800,000 | 1,25% | ||

| 7 | 7,500,001 to 8,550,000 | 1,50% | 10,750,001 to 11,250,000 | 2,00% | 9,800,001 to 10,950,000 | 1,50% | ||

| 8 | 8,550,001 to 9,650,000 | 1,75% | 11,250,001 to 11,600,000 | 2,50% | 10,950,001 to 11,200,000 | 1,75% | ||

| 9 | 9,650,001 to 10,050,000 | 2,00% | 11,600,001 to 12,600,000 | 3,00% | 11,200,001 to 12,050,000 | 2,00% | ||

| 10 | 10,050,001 to 10,350,000 | 2,25% | 12,600,001 to 13,600,000 | 4,00% | 12,050,001 to 12,950,000 | 3,00% | ||

| 11 | 10,350,001 to 10,700,000 | 2,50% | 13,600,001 to 14,950,000 | 5,00% | 12,950,001 to 14,150,000 | 4,00% | ||

| 12 | 10,700,001 to 11,050,000 | 3,00% | 14,950,001 to 16,400,000 | 6,00% | 14,150,001 to 15,550,000 | 5,00% | ||

| 13 | 11,050,001 to 11,600,000 | 3,50% | 16,400,001 to 18,450,000 | 7,00% | 15,550,001 to 17,050,000 | 6,00% | ||

| 14 | 11,600,001 to 12,500,000 | 4,00% | 18,450,001 to 21,850,000 | 8,00% | 17,050,001 to 19,500,000 | 7,00% | ||

| 15 | 12,500,001 to 13,750,000 | 5,00% | 21,850,001 to 26,000,000 | 9,00% | 19,500,001 to 22,700,000 | 8,00% | ||

| 16 | 13,750,001 to 15,100,000 | 6,00% | 26,000,001 to 27,700,000 | 10,00% | 22,700,001 to 26,600,000 | 9,00% | ||

| 17 | 15,100,001 to 16,950,000 | 7,00% | 27,700,001 to 29,350,000 | 11,00% | 26,600,001 to 28,100,000 | 10,00% | ||

| 18 | 16,950,001 to 19,750,000 | 8,00% | 29,350,001 to 31,450,000 | 12,00% | 28,100,001 to 30,100,000 | 11,00% | ||

| 19 | 19,750,001 to 24,150,000 | 9,00% | 31,450,001 to 33,950,000 | 13,00% | 30,100,001 to 32,600,000 | 12,00% | ||

| 20 | 24,150,001 to 26,450,000 | 10,00% | 33,950,001 to 37,100,000 | 14,00% | 32,600,001 to 35,400,000 | 13,00% | ||

| 21 | 26,450,001 to 28,000,000 | 11,00% | 37,100,001 to 41,100,000 | 15,00% | 35,400,001 to 38,900,000 | 14,00% | ||

| 22 | 28,000,001 to 30,050,000 | 12,00% | 41,100,001 to 45,800,000 | 16,00% | 38,900,001 to 43,000,000 | 15,00% | ||

| 23 | 30,050,001 to 32,400,000 | 13,00% | 45,800,001 to 49,500,000 | 17,00% | 43,000,001 to 47,400,000 | 16,00% | ||

| 24 | 32,400,001 to 35,400,000 | 14,00% | 49,500,001 to 53,800,000 | 18,00% | 47,400,001 to 51,200,000 | 17,00% | ||

| 25 | 35,400,001 to 39,100,000 | 15,00% | 53,800,001 to 58,500,000 | 19,00% | 51,200,001 to 55,800,000 | 18,00% | ||

| 26 | 39,100,001 to 43,850,000 | 16,00% | 58,500,001 to 64,000,000 | 20,00% | 55,800,001 to 60,400,000 | 19,00% | ||

| 27 | 43,850,001 to 47,800,000 | 17,00% | 64,000,001 to 71,000,000 | 21,00% | 60,400,001 to 66,700,000 | 20,00% | ||

| 28 | 47,800,001 to 51,400,000 | 18,00% | 71,000,001 to 80,000,000 | 22,00% | 66,700,001 to 74,500,000 | 21,00% | ||

| 29 | 51,400,001 to 56,300,000 | 19,00% | 80,000,001 to 93,000,000 | 23,00% | 74,500,001 to 83,200,000 | 22,00% | ||

| 30 | 56,300,001 to 62,200,000 | 20,00% | 93,000,001 to 109,000,000 | 24,00% | 83,200,001 to 95,600,000 | 23,00% | ||

| 31 | 62,200,001 to 68,600,000 | 21,00% | 109,000,001 to 129,000,000 | 25,00% | 95,600,001 to 110,000,000 | 24,00% | ||

| 32 | 68,600,001 to 77,500,000 | 22,00% | 129,000,001 to 163,000,000 | 26,00% | 110,000,001 to 134,000,000 | 25,00% | ||

| 33 | 77,500,001 to 89,000,000 | 23,00% | 163,000,001 to 211,000,000 | 27,00% | 134,000,001 to 169,000,000 | 26,00% | ||

| 34 | 89,000,001 to 103,000,000 | 24,00% | 211,000,001 to 374,000,000 | 28,00% | 169,000,001 to 221,000,000 | 27,00% | ||

| 35 | 103,000,001 to 125,000,000 | 25,00% | 374,000,001 to 459,000,000 | 29,00% | 221,000,001 to 390,000,000 | 28,00% | ||

| 36 | 125,000,001 to 157,000,000 | 26,00% | 459,000,001 to 555,000,000 | 30,00% | 390,000,001 to 463,000,000 | 29,00% | ||

| 37 | 157,000,001 to 206,000,000 | 27,00% | 555,000,001 to 704,000,000 | 31,00% | 463,000,001 to 561,000,000 | 30,00% | ||

| 38 | 206,000,001 to 337,000,000 | 28,00% | 704,000,001 to 957,000,000 | 32,00% | 561,000,001 to 709,000,000 | 31,00% | ||

| 39 | 337,000,001 to 454,000,000 | 29,00% | 957,000,001 to 1,405,000,000 | 33,00% | 709,000,001 to 965,000,000 | 32,00% | ||

| 40 | 454,000,001 to 550,000,000 | 30,00% | above 1,405,000,000 | 34,00% | 965,000,001 to 1,419,000,000 | 33,00% | ||

| 41 | 550,000,001 to 695,000,000 | 31,00% | above 1,419,000,000 | 34,00% | ||||

| 42 | 695,000,001 to 910,000,000 | 32,00% | ||||||

| 43 | 910,000,001 to 1,400,000,000 | 33,00% | ||||||

| 44 | above 1,400,000,000 | 34,00% | ||||||

How to use the income tax calculation formula?

If you pay your employee a bonus, add it to their salary in the respective month to increase gross income, then apply the effective rate corresponding to the gross income as shown in the table. So, it is no longer possible to separate PPh 21 on salary and bonus using the new tax regulation in Indonesia.

2. Progressive rate

The progressive rate is an individual income tax rate regulated in UU PPh, Article 17, Paragraph 1. The rates are levied on taxable income (PKP) — net income minus PTKP. Net income is gross income minus occupational expenses and pension premiums.

| Layer | Taxable Income (Rp) | Rate |

|---|---|---|

| 1 | Up to 60,000,000 | 5% |

| 2 | 60,000,001 to 250,000,000 | 15% |

| 3 | 250,000,001 to 500,000,000 | 25% |

| 4 | 500,000,001 to 5,000,000,000 | 30% |

| 5 | Above 5,000,000,000 | 35% |

The higher the taxable income, the higher the income tax rate. For example, taxable income up to Rp60,000,000 is only subject to one layer of the rate, which is 5%. But if the PKP is Rp70,000,000, then it is subject to two layers of rates, specifically 5% for Rp60,000,000 and 15% for Rp10,000,000.

In the latest tax regulation, the progressive rate only applies to calculate the annual income tax — PPh 21 tax withholding in December or the last month before the employee resigns or quits.

It is not possible to use the progressive rate for monthly tax withholding. Instead, you should apply the effective rate to calculate PPh 21 from January to November.

Also Read: Income Tax in Indonesia for Foreign Businesses

Bonus payment before December

Let us look at an example of bonus tax withholding in a month other than December. As explained above, you must apply the effective rate to calculate a monthly income tax withholding.

Here is how:

- Add bonus and other payments, if any, to salary to get total gross income;

- Determine the PTKP of the employee;

- Select the table that matches to the PTKP;

- Find the correct rate that corresponds to the total gross income;

- Use the formula to calculate PPh 21;

- The after-tax earnings or take-home pay (THP) is the gross income minus PPh 21.

Let us say you pay an employee a salary of Rp15,000,000 plus an annual bonus of Rp20,000,000 in the January payroll. The employee is married and has two children. How much tax should you deduct from the payslip? How much is his THP?

Here is the answer:

1. His gross income is salary plus bonus

| Gross Income | = Salary + bonus = Rp15,000,000 + Rp20,000,000 = Rp35,000,000 |

2. The employee status is married and has two children, so PTKP K/2 applies

3. For the PTKP K/2 tax rates, you have to look at the table of Category B

4. For a total gross income of Rp35,000,000, you will find rate no. 20, which is 14%

5. The PPh 21 deduction is:

| PPh 21 | = Effective rate x Gross income = 14% x Rp35,000,000 = Rp4,900,000 |

6. The after-tax income is:

| After-tax income | = Gross income – PPh 21 = Rp35,000,000 – Rp4,900,000 = Rp30,100,000 |

Bonus payment in December

If you pay your employee an annual bonus in December, the tax calculation will differ from monthly tax withholding. You should apply the progressive rate instead of the effective rate.

From the example above, let us calculate tax deductions from January to November. The employee receives gross income without a bonus as much as the salary (Rp15,000,000).

If you search in the Category B table, you will find rate no. 12 for gross income of Rp15,000,000, which is 6%.

| PPh 21 | = Effective rate x Gross income = 6% x Rp15,000,000 = Rp900,000 |

If the gross income amount is fixed, the sum of tax withholding from January to November is as follows:

| Month | Gross Income | PPh 21 (Rp) | PPh 21 Cumulative (Rp) | |

| Salary (Rp) | Bonus (Rp) | |||

| January | 15,000,000 | – | 900,000 | 900,000 |

| February | 15,000,000 | – | 900,000 | 1,800,000 |

| March | 15,000,000 | – | 900,000 | 2,700,000 |

| April | 15,000,000 | – | 900,000 | 3,600,000 |

| May | 15,000,000 | – | 900,000 | 4,500,000 |

| June | 15,000,000 | – | 900,000 | 5,400,000 |

| July | 15,000,000 | – | 900,000 | 6,300,000 |

| August | 15,000,000 | – | 900,000 | 7,200,000 |

| September | 15,000,000 | – | 900,000 | 8,100,000 |

| October | 15,000,000 | – | 900,000 | 9,000,000 |

| November | 15,000,000 | – | 900,000 | 9,900,000 |

| December | 15,000,000 | 20,000,000 | ? | ? |

| TOTAL | 180,000,000 | 20,000,000 | ? | ? |

In the last month of the fiscal year, you will withhold tax levied on the annual gross income, including bonus. But first, you have to calculate the amount of PTKP K/3 as follows:

| Non-taxable income | Amount (Rp) |

|---|---|

| Personal PTKP | 54,000,000 |

| Additional amount for a wife | 4,500,000 |

| Additional amount for having two dependents (4,500,000 for each) | 9,000,000 |

| PTKP K/3 | 67,500,000 |

Then, calculate the annual income tax by applying the progressive rates like the example below:

| PPh 21 Calculation (Rp) | ||

|---|---|---|

| Total annual salary | 180,000,000 | |

| Bonus | 20,000,000 | |

| Gross income | 200,000,000 | |

| Occupational expenses 5% of gross income (max, 6,000,000) | 6,000,000 | |

| Pension premium in a year12 x 100,000 | 1,200,000 | |

| Total deduction | -7,200,000 | |

| Net income | 192,800,000 | |

| Non-taxable income (PTKP) K/3 | -67,500,000 | |

| Taxable income (PKP) | 125,300,000 | |

| PPh 21Rate layer 1 (5% x 60,000,000) Rate layer 2 (15% x 65,300,000) | 3,000,0009,795,000 | |

| Total annual tax | 12,795,000 | |

| PPh 21 withholding from Jan to Nov | -9,900,000 | |

| PPh 21 deducted in December | 2,895,000 |

So, PPh 21 on salary and bonus in December is the annual tax minus the total PPh 21 deducted within 11 months before. After the end of the fiscal year, the employee should report their salary, bonus, allowance, overtime, and other payments earned in a year when they file personal Annual Tax Return (SPT).

Also Read: NPWP: Key to Tax Compliance in Indonesia

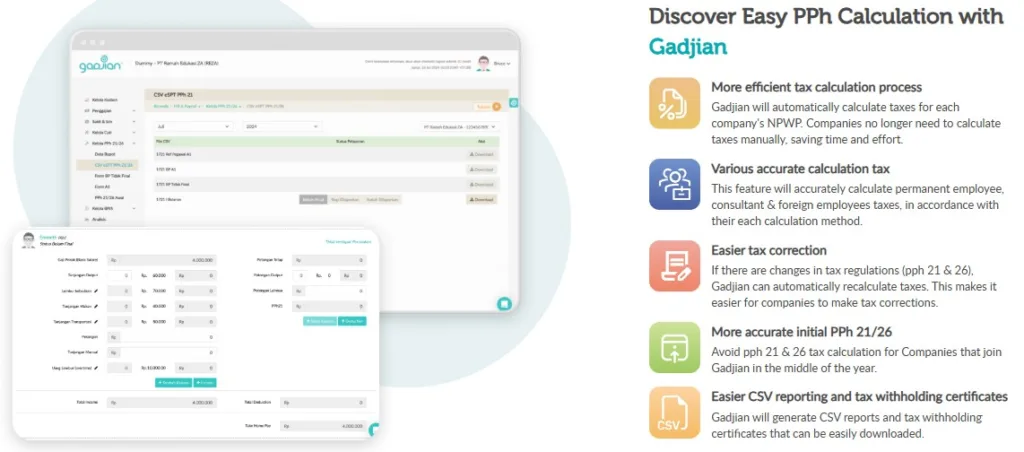

The best tool to automate your payroll system

Is a payroll job burdensome for you? Make it easy with Gadjian, the best web-based payroll software in Indonesia. You can streamline your periodic payroll tasks efficiently by an automatic calculation system. Totalizing payroll components and preparing payslips are no longer enervating tasks. This cloud tool allows you to complete your company payroll anywhere and anytime.

Gadjian has a faultless salary and bonus calculator. The tool also effortlessly reckons other income such as allowances, overtime pay, and social security insurance premiums (BPJS).

For efficiency, this software also comes with an error-free tax application to count up tax deductions on payslips automatically. So, you don’t need to use a separate tax software that adds costs. With Gadjian, you can complete your payroll tasks in minutes, from calculation to disbursement.

Gadjian tax calculator can smartly count up resident taxpayer income tax (PPh 21) for contract and permanent employees. Are you hiring foreign employees? This app can also calculate non-resident taxpayer income tax (PPh 26), whether or not they are from a tax treaty partner country with Indonesia.

Do not worry about the tool’s accuracy. The software computation methods are set to comply with the latest regulations in Indonesia, such as social security, taxes, and labor law. Whenever the government amends the rules affecting payroll systems in the private sector, we will update the app to make adjustments for you.

Gadjian is a versatile Software as a Service (SaaS) for HRD. It also helps you manage the recruitment process, control your business inventories and assets, and monitor your employee performance.

Sumber